Date: Mar 2026

Gold has long been regarded as a reliable store of value. Investors across the world turn to the metal in times of uncertainty, inflationary cycles and periods of monetary instability. However, because gold is globally traded and priced in US dollars, its performance varies significantly depending on the currency of measurement. For Indian investors, gold is not just a commodity, it’s a currency-linked asset. The interplay between USD, INR and Gold prices creates a smoother, more stable experience in rupees, primarily through reduced volatility rather than chasing higher returns.

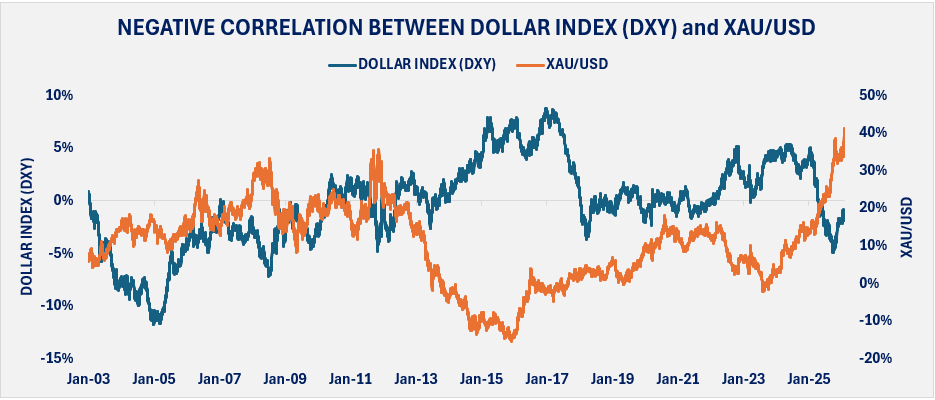

Globally, gold is priced in USD which means movements in the currency play a critical role in determining gold’s international price.

Source: Investing.com (Data as on 31st January 2026)

As shown above, we analysed daily 3-year rolling returns since January 2000 and observed a strong inverse relationship between the US Dollar Index (DXY) and Gold (USD): returns exhibited a negative correlation of 60%. This is due to the fact that when the Dollar Index rises and the US dollar gets stronger, gold becomes more expensive for buyers outside the US, so demand drops. Contrarily, a weaker dollar makes gold more affordable worldwide, surging demand and sparking price rallies. The relationship exists because gold is viewed as an alternative monetary asset. A strong dollar reduces the need for currency hedging, while a weakening dollar typically increases demand for gold as a store of value. This dynamic is important when evaluating gold returns from a global investor’s perspective. However, Indian investors experience an additional layer of complexity due to INR conversion.

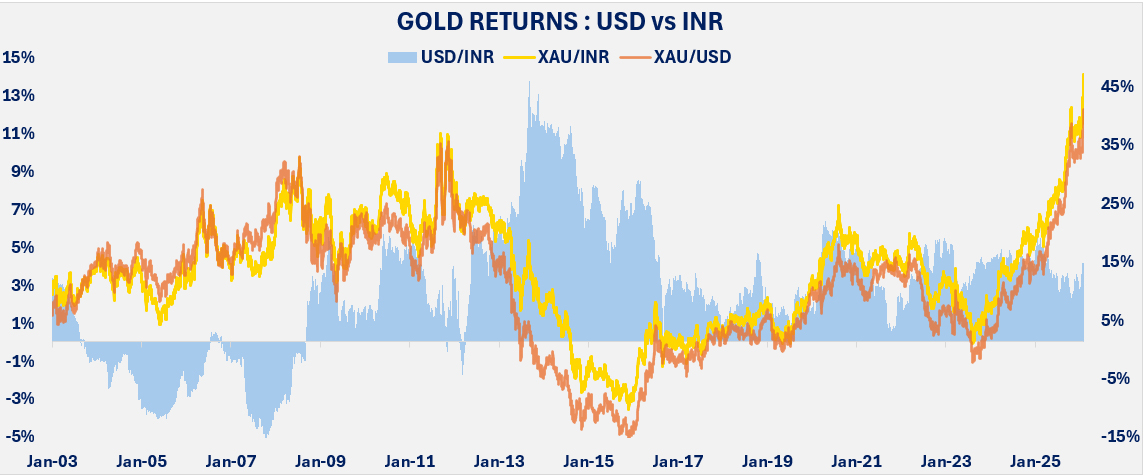

Gold’s daily global price is set in USD per troy ounce (~31.1035 grams) via the London auction. In India, this converts to INR at the prevailing USD-INR rate, plus import duties, shipping, and taxes. Gold INR thus hinges on two variables: USD gold prices and USD-INR. When the dollar gets stronger, the rupee gets weaker. A weaker rupee makes gold cost more in rupees. This extra cost helps balance out any fall in the dollar price of gold. The same happens vice versa when the dollar gets weaker.

Source: Investing.com (Data as on 31st January 2026)

As shown above, we analysed the daily 3-year rolling returns for Gold INR and Gold USD across the USD-INR relationship with data commencing from January 2000. The rupee’s gradual depreciation acts as a consistent tailwind, cushioning global corrections and slashing volatility for Indian holders. Gold USD has seen negative return periods with sharper swings, while gold INR experiences relatively milder ones. For instance, during 2011-2012, Gold USD dropped 10-15% but the rupee depreciation muted the impact, delivering modest stability instead of steep losses.

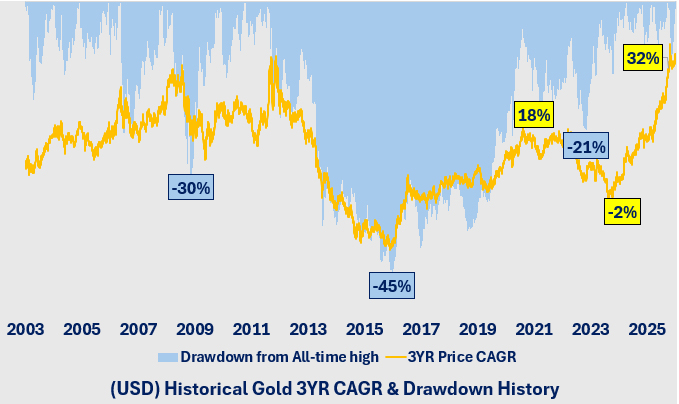

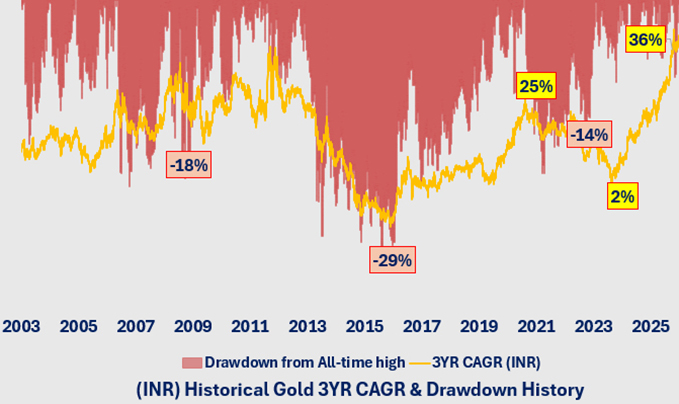

Drawdowns measure the peak-to-trough decline in an asset, capturing the depth of temporary losses before recovery. When plotted side by side, the contrast between USD and INR gold is evident. As shown below, gold priced in USD has faced far deeper drawdowns, including a steep fall of about 45% around 2015, alongside major declines of 30% in 2008-09 and 21% in 2022. In comparison, gold INR saw a maximum drawdown of only around 29%, 18% and 14% in those same periods respectively. The rupee’s steady depreciation offsets part of the global gold price declines, cushioning Indian investors from the full extent of market stress. This currency effect creates a visibly smoother drawdown curve in INR terms, highlighting why gold behaves as a more stable wealth preserver for domestic investors. Data confirm that for Indian investors, gold prices in rupees tend to deliver a smoother and more stable return profile over the long term.

Source: Investing.com (Data as on 31st January 2026)

Source: Investing.com (Data as on 31st January 2026)

For Indian investors, holding gold priced in INR has historically offered a more stabilised experience compared to a pure USD exposure. The natural depreciation of the rupee foreign exchange rate acts as a buffer that reduces downside risks and volatility. At Privus Advisors, we view gold not as a high return asset but as a strategic diversifier that balances equity risk, preserves purchasing power, and offers stability during volatile phases. Understanding gold’s currency dynamics allows investors to better position it within a diversified portfolio, measured in their local currency.

DISCLAIMER: This report/presentation is intended for the personal and private use of the recipient and is for private circulation only. It is not to be published, reproduced, distributed, or disclosed, whether wholly or in part, to any other person or entity without prior written consent. The report/presentation has been prepared by Privus Advisors (Firm) based on the information available in public domain & other external sources which are beyond Privus’ control and may also include the Firm’s personal views. Though the recipient recognizes such information to be generally reliable, the recipient acknowledges that inaccuracies may occur & that the Firm does not warrant the accuracy or suitability of the information. Neither does the information nor any opinion expressed constitute a legal opinion or an offer, or an invitation to make an offer, to buy or sell any financial or other products / services or securities or any kind of derivatives related to such securities. Any information contained herein relating to taxation is based on the information available in the public domain that may be subject to change. Investors/Clients should refer to relevant foreign exchange regulations / taxation / financial advice as applicable in India and/or abroad about the appropriateness and relevance / impact of the views or suggestions expressed herein, related to any Investment/Estate Planning / Succession Planning. All investments are subject to market risks, read all related documents carefully before investing. The Firm is registered with SEBI as a non-individual RIA bearing Reg. No. INA000019752 & BSEASL membership No. 2230. Registration granted by SEBI, membership of BASL and certification of National Institute of Securities Markets (NISM) in no way guarantees performance of the intermediary or provide any assurance of returns to investors.