Date: May 2026

For decades, Indian investors have rightly viewed India as a compelling long-term wealth creation opportunity, supported by strong demographics, rising consumption and structural economic growth. However, as wealth grows, portfolio construction must evolve beyond familiarity. Wealth management is not merely about participating in a single growth story, but about building resilient portfolios across geographies, currencies and market cycles. This is why the world’s largest institutional investors and family offices diversify globally, not because they lack conviction in their home markets, but because they recognise that market leadership changes over time. Most investors around the world exhibit “home bias”, a behavioural tendency to allocate disproportionately towards domestic markets because they feel familiar and understandable. Indian investors are no exception. Strong domestic equity performance in recent years has further reinforced this comfort, leaving most portfolios heavily concentrated in Indian equities despite India representing only 3-3.5% of global market capitalisation. While portfolios may appear diversified across sectors and market caps, they still remain dependent on a single economy, currency, regulatory framework, and market cycle.

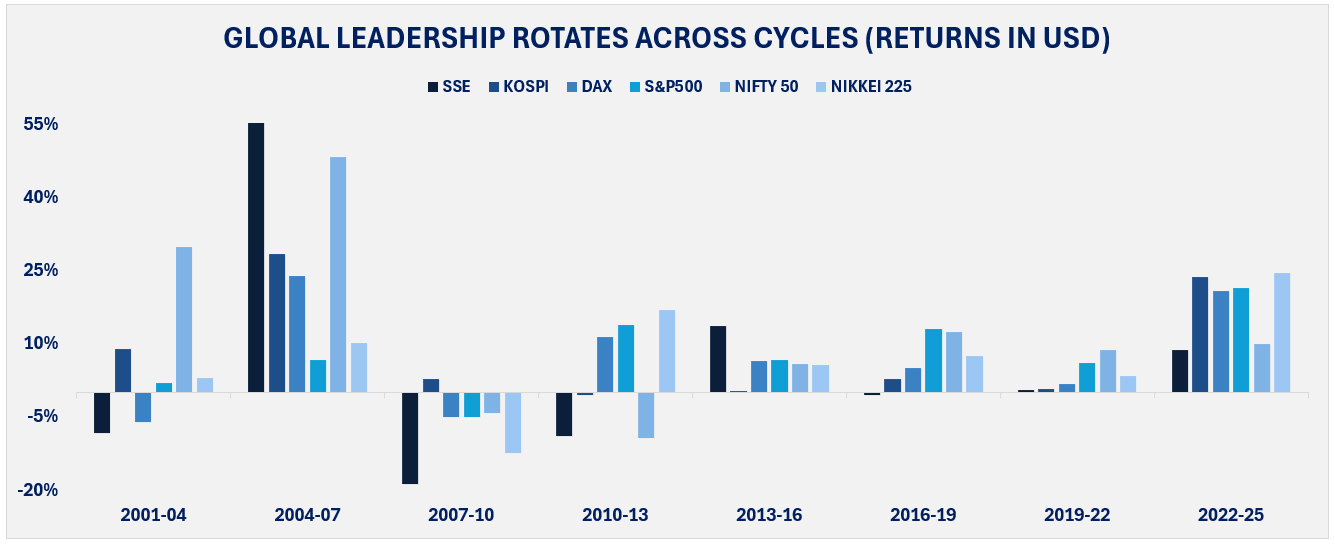

Different markets are driven by fundamentally different economic structures, and this manifests visibly in how their return cycles diverge over time. In 2001 to 2004, India led the pack decisively with the Nifty 50 delivering 30% returns, well ahead of Korea at 9% and Japan at 3%, while China, Germany and the S&P 500 all struggled to generate meaningful positive returns. The 2004 to 2007 cycle was decisively China’s, with the SSE delivering 61% returns, dwarfing every other market and standing as the single strongest period performance, with India coming in second at 48% and Korea at 28%, while the S&P 500 lagged the group at just 7%. The 2007 to 2010 cycle was broadly painful across geographies, with China bearing the steepest loss at 19%, Japan falling 13%, and Germany and the S&P 500 both down 5%, while South Korea was the relative standout, losing just 3%. In 2010 to 2013, Japan led with 17% returns and the S&P 500 followed at 14%, while China and India were the clear laggards, both falling 9%. In 2013 to 2016, China quietly took the lead at 14%, with the S&P 500 at 7% and Germany at 6% close behind, while South Korea delivered flat returns at 0%. The 2016 to 2019 cycle saw the S&P 500 edge ahead at 13%, with India close behind at 12%, while China was the only market to post a negative return at 1%. In 2019 to 2022, returns were broadly muted across all markets with India leading modestly at 9% and the S&P 500 at 6%, while China and Korea delivered effectively flat returns. The most recent 2022 to 2025 cycle has been notably broad based, with Korea, Japan, Germany and the S&P 500 all posting strong returns of around 21 to 24%, while China and India, despite positive returns of 9% and 10% respectively, have been the relative laggards of this cycle. The S&P 500, uniquely, has delivered positive returns across every single period on the chart, making it the most consistent compounder even if it has rarely been the outright leader in any single cycle.

No single market has dominated across all periods and leadership has rotated consistently, which is precisely why a portfolio concentrated in any one geography will inevitably miss the periods when others are leading the cycle.

The longer markets are held, the more stable their return profiles tend to become, but stability is only part of the story. The real opportunity lies in the upside generated during powerful market cycles. Over rolling 3-year periods, India and China have delivered maximum annualised returns of 62% and 66% respectively against medians of just 9% and 1%, while South Korea has reached as high as 48% against a median of 5%. Even more, developed markets have produced exceptional cycles, with Nikkei reaching 35%, Germany 38% and the S&P 500 27%, against medians of 8%, 8% and 9% respectively. These cycles typically emerge when policy support, earnings growth, sector leadership and currency trends align simultaneously, creating multi-year compounding opportunities that are often recognised only in hindsight. A portfolio concentrated in a single market participates only in its domestic cycle, while a globally diversified portfolio gains exposure to these leadership shifts as they emerge across different regions and economic environments.

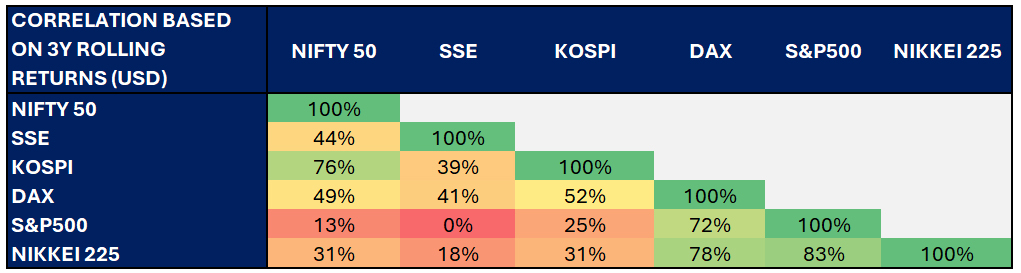

One of the most important but least discussed concepts in portfolio construction is correlation, which measures how different markets move relative to each other. Diversification is not merely about owning different assets but owning assets that behave differently across market environments. Historically, India’s correlation with global markets has risen over time due to increasing integration with global capital flows, however, meaningful differences still exist. These markets do not outperform or underperform in lockstep with India and that divergence itself becomes a source of portfolio stability.

Source: Investing.com (3Y rolling returns based on data from 2001-2026)

Markets like KOSPI, with a 76% correlation to Nifty, tend to move in a similar direction during broad risk on cycles, meaning that when global growth accelerates and investor sentiment is strong, both markets participate meaningfully in the upside together. At the same time, markets like the S&P 500, with a low 13% correlation to Nifty 50, are driven by entirely different structural forces, innovation, technology and global consumer spending, meaning their strongest periods often emerge independently of what is driving India. SSE at 44%, Germany at 49% and Nikkei at 31% sit between these two extremes, each offering partial independence from Indian market cycles while still participating in global growth environments. The result is a portfolio that is not forced to choose between growth and stability. When global risk appetite is high, correlated markets amplify returns together. When India faces a domestic headwind, low correlation markets continue compounding to their own cycle. A globally diversified portfolio is therefore not a defensive construct but an offensive one, designed to ensure that there is always a part of the portfolio compounding meaningfully regardless of where we are in the global economic cycle.

All the above analysis is in USD terms; for an Indian investor, the structural rupee depreciation against the dollar adds an additional layer of return on top, making the case even more compelling. Over the last 2 decades the rupee has depreciated against the dollar at 3% annually, and while this may appear unfavourable in isolation, it meaningfully enhances returns for Indian investors holding global assets. Global diversification is therefore not merely geographical but also a form of currency diversification, offering simultaneous exposure to global businesses, stronger reserve currencies and growth cycles that operate independently of the domestic economy.

As wealth grows, preserving global purchasing power becomes as important as generating returns. Affluent families increasingly carry global education expenses and liabilities linked to foreign currencies, yet most portfolios remain entirely rupee denominated. Global investing addresses that structural mismatch while also providing access to sectors that simply do not exist domestically. An investor seeking exposure to global AI leadership, semiconductor manufacturing or enterprise software cannot achieve this within Indian markets alone. When the rupee depreciates, as it structurally has over decades, global assets held in stronger currencies quietly appreciate in rupee terms, providing a natural hedge against the erosion of domestic purchasing power. Equally, because global markets operate on different cycles and respond to different economic drivers, a diversified portfolio tends to experience more contained losses during periods of domestic stress, as losses in one market are partially offset by stability or gains elsewhere. The result is not just a smoother ride but a structurally more resilient portfolio that recovers faster and compounds more consistently over time. Ultimately, global diversification is not an argument against India, which remains one of the most compelling long term growth stories in the world. It is simply the recognition that a globally diversified portfolio allows investors to participate in India’s structural growth alongside the best of what the rest of the world has to offer, while ensuring that no single economy, currency or market cycle carries the entire weight of long-term wealth preservation.

At Privus Advisors, we believe portfolio construction should reflect the realities of an increasingly interconnected world. Global diversification is not about chasing international trends or tactical opportunities. It is about building structurally stronger portfolios capable of navigating changing market cycles, economic regimes and currency environments over long periods of time. Because wealth preservation is rarely achieved through concentration alone. More often, it is achieved through thoughtful diversification, disciplined allocation, and the ability to look beyond familiar borders.

DISCLAIMER: This report/presentation is intended for the personal and private use of the recipient and is for private circulation only. It is not to be published, reproduced, distributed, or disclosed, whether wholly or in part, to any other person or entity without prior written consent. The report/presentation has been prepared by Privus Advisors (Firm) based on the information available in public domain & other external sources which are beyond Privus’ control and may also include the Firm’s personal views. Though the recipient recognizes such information to be generally reliable, the recipient acknowledges that inaccuracies may occur & that the Firm does not warrant the accuracy or suitability of the information. Neither does the information nor any opinion expressed constitute a legal opinion or an offer, or an invitation to make an offer, to buy or sell any financial or other products / services or securities or any kind of derivatives related to such securities. Any information contained herein relating to taxation is based on the information available in the public domain that may be subject to change. Investors/Clients should refer to relevant foreign exchange regulations / taxation / financial advice as applicable in India and/or abroad about the appropriateness and relevance / impact of the views or suggestions expressed herein, related to any Investment/Estate Planning / Succession Planning. All investments are subject to market risks, read all related documents carefully before investing. The Firm is registered with SEBI as a non-individual RIA bearing Reg. No. INA000019752 & BSEASL membership No. 2230. Registration granted by SEBI, membership of BASL and certification of National Institute of Securities Markets (NISM) in no way guarantees performance of the intermediary or provide any assurance of returns to investors.