Date: April 2025

A long-standing debate in investing is whether it is better to time the market or to have time in the market. While the latter is frequently touted as the more reliable strategy, a nuanced perspective reveals that both concepts hold significant weight in achieving optimal investment outcomes. It’s a tango between strategic entry and persistent patience rather than an either-or choice.

‘Timing the market’ refers to the strategy of attempting to predict future market movements to buy low and sell high. The allure is obvious: perfectly timed trades can lead to significant and rapid gains. The returns could be enormous if you imagine buying at the absolute bottom of a market downturn and selling at the peak of a bull run. However, the reality is that most investors find it challenging, if not impossible, to consistently and accurately time the market. ‘Time in the market’, on the other hand, emphasizes the importance of holding onto your investment for the long haul, no matter what happens in the short term in the markets. This strategy takes advantage of the compounding force that results in your earnings on your investment create additional earnings over time, creating compounding growth.

Although “time in the market” is usually the foundation of effective long-term investing, discounting the “timing” factor altogether might lose opportunities or suboptimal entry points. The best case usually comes with a calculated way of when and how you enter the market and then patience to allow time to work.

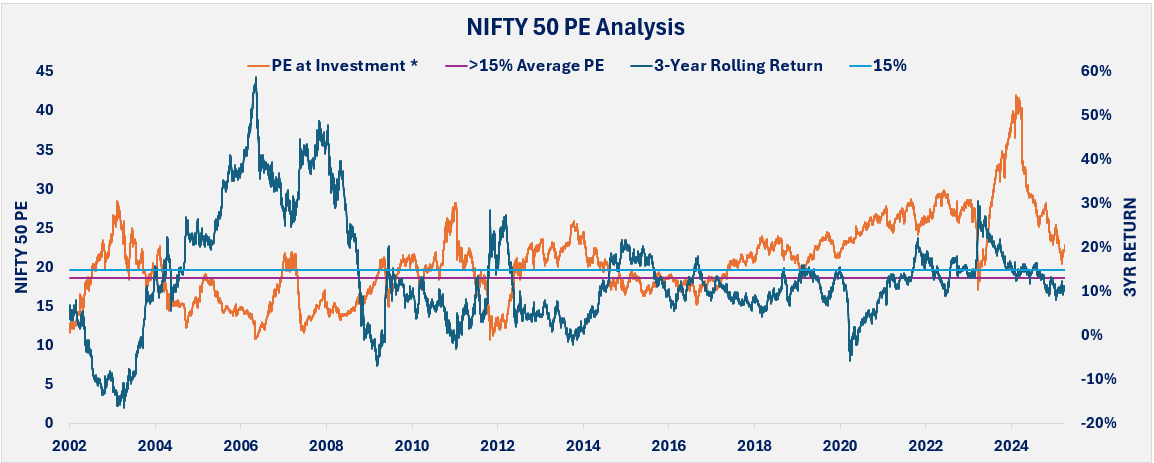

Analysing the rolling returns of the NIFTY 50 gives useful insights into the effect of investment time horizon on volatility. Rolling returns give a more stable view than point-to-point returns, which can be greatly affected by the start and end dates chosen.

Source: NSE (Data as on 31st March 2025)

Rolling return analysis shows that as the holding period increases from 1 to 3 & 5 years, volatility in returns tends to reduce. Those that remain invested through market cycles will benefit from the long-term upward trend of the market and are less likely to be negatively impacted by temporary downturns.

Interestingly, the same examination of a 3-year holding period also shows that there is a 34% chance of an investor making an extra 20% of the average return when entering the market on these particular days. Since 1996, the average 3-year rolling return achieved by the Nifty 50 is 12.2%. Further insights regarding potential outcomes can be obtained through valuation metrics such as the Price-to-Earnings (PE) ratio. For instance, when the NIFTY 50 is positioned at a PE of 18x – 20x, the probability of experiencing negative returns over a threeyear investment horizon decreases from 9% to around 1%, indicating an 88% reduction in downside risk, highlighting the possibility of improving rewards through entry into the market at more moderate valuations.

It is essential to recognize that this does not promote zealous market timing in hopes of finding these “lucky” days. Rather, this information serves to reinforce the point we mentioned previously: paying attention to overall market conditions and valuations can make an impact on long-term returns. Although consistently predicting these high-probability entry points is impossible, understanding that market cycles exist and being ready to invest when valuations are reasonable can help you somewhat improve your odds over time.

Ultimately, the most successful investment journey is often a marathon, not a sprint. By focusing on long-term participation while respecting strategic points of entry, investors can use the power of both timing and time to

accomplish monetary objectives.

DISCLAIMER: This report/presentation is intended for the personal and private use of the recipient and is for private circulation only. It is not to be published, reproduced, distributed, or disclosed, whether wholly or in part, to any other person or entity without prior written consent. The report/presentation has been prepared by Privus Advisors (Firm) based on the information available in public domain & other external sources which are beyond Privus’ control and may also include the Firm’s personal views. Though the recipient recognizes such information to be generally reliable, the recipient acknowledges that inaccuracies may occur & that the Firm does not warrant the accuracy or suitability of the information. Neither does the information nor any opinion expressed constitute a legal opinion or an offer, or an invitation to make an offer, to buy or sell any financial or other products / services or securities or any kind of derivatives related to such securities. Any information contained herein relating to taxation is based on the information available in the public domain that may be subject to change. Investors/Clients should refer to relevant foreign exchange regulations / taxation / financial advice as applicable in India and/or abroad about the appropriateness and relevance / impact of the views or suggestions expressed herein, related to any Investment/Estate Planning / Succession Planning. All investments are subject to market risks, read all related documents carefully before investing. The Firm is registered with SEBI as a non-individual RIA bearing Reg. No. INA000019752 & BSEASL membership No. 2230. Registration granted by SEBI, membership of BASL and certification of National Institute of Securities Markets (NISM) in no way guarantees performance of the intermediary or provide any assurance of returns to investors.